The Prevalence of Valuation Caps in SAFEs (Before a Priced Round)

.avif)

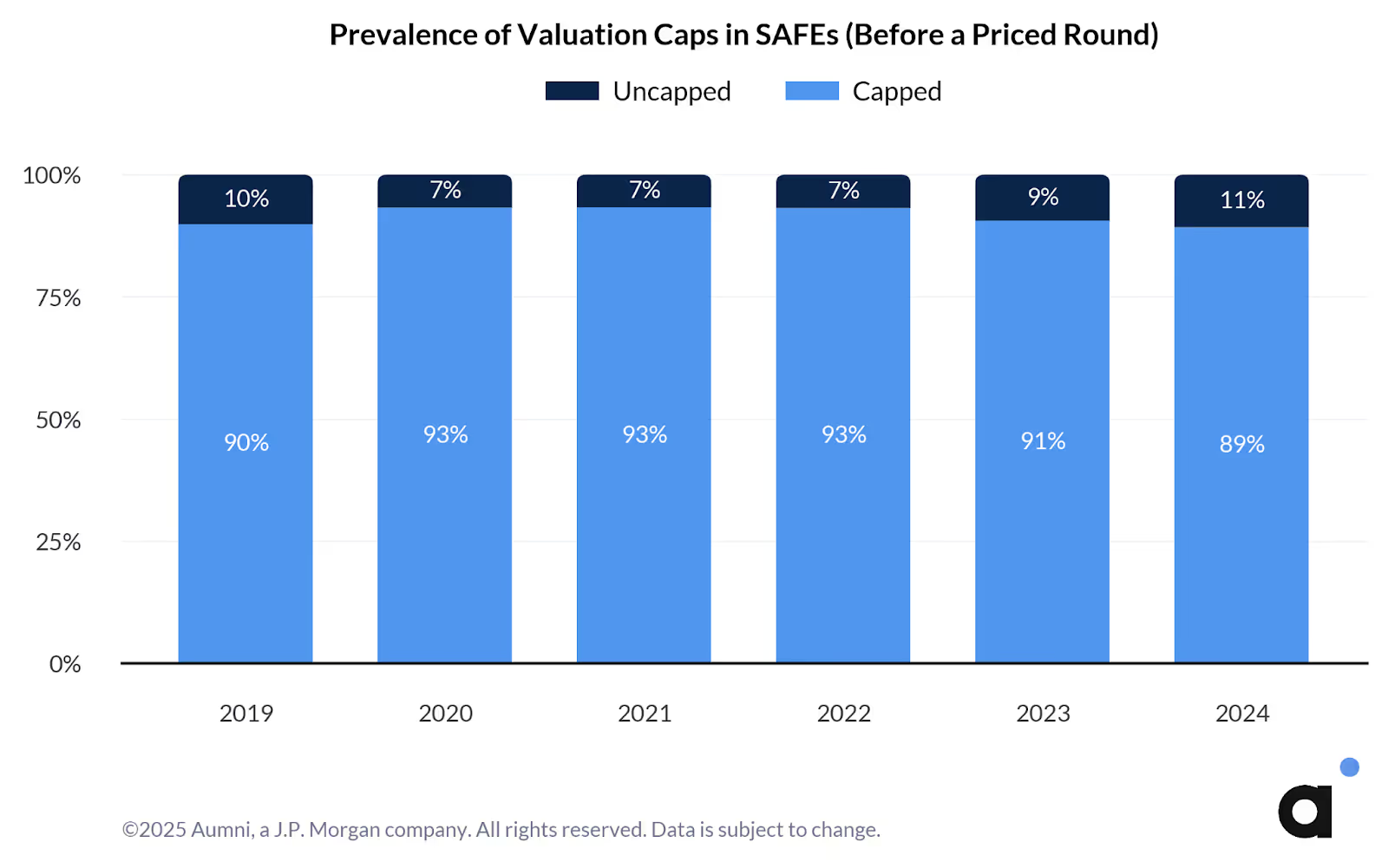

SAFEs are the most common convertible instrument for startups looking for capital before priced equity rounds. While the use of Uncapped SAFEs (those issued without a valuation cap) has traditionally been less common, there has been a slight uptick in their prevalence in recent years. Between 2020 and 2024, the prevalence of pre-priced round SAFEs issued without a valuation cap increased from 7% to 11%.

A valuation cap sets the maximum valuation at which a convertible instrument will convert to equity regardless of the company’s actual valuation when it raises a priced round. Valuation caps are often seen as investor-friendly provisions as they protect investors from dilution in the event that the company raises its priced round at a very high valuation. However, the recent uptick in the frequency of uncapped SAFEs could potentially indicate a lack of certainty in the valuation environment, which has been choppy over the last few years.

For example, say an investor invests $500,000 through a SAFE with a $20 million valuation cap. Setting other variables aside for purposes of the example, the investor has secured at least a 2.5% stake in the company. Here is what happens in three scenarios:

Scenario 1 — Valuation under cap: If the company raises a priced round at a $10 million post-money valuation, the valuation cap has not been met and the SAFE will convert at $10 million giving the investor 5% ownership.

Scenario 2 — Valuation over cap: If the company raises a priced round at a $25 million valuation, the valuation cap has been met and the SAFE will convert at $20 million giving the investor 2.5% ownership.

Scenario 3 — Uncapped SAFE: If the SAFE was purchased at the same $500,000 but without a valuation cap and the company raised a priced round at a $25 million valuation, the investor would only receive a 2% stake in the company.

Looking for more venture data?

©2025 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC.

This material is not the product of J.P. Morgan’s Research Department. It is not a research report and is not intended as such. This material is provided for informational purposes only and is subject to change without notice. It is not intended as research, a recommendation, advice, offer or solicitation to buy or sell any financial product or service, or to be used in any way for evaluating the merits of participating in any transaction. Please consult your own advisors regarding legal, tax, accounting or any other aspects including suitability implications, for your particular circumstances or transactions. J.P. Morgan and its third-party suppliers disclaim any responsibility or liability whatsoever for the quality, fitness for a particular purpose, non-infringement, accuracy, currency or completeness of the information herein, and for any reliance on, or use of this material in any way. Any information or analysis in this material purporting to convey, summarize, or otherwise rely on data may be based on a sample or normalized set thereof. This material is provided on a confidential basis and may not be reproduced, redistributed or transmitted, in whole or in part, without the prior written consent of J.P. Morgan. Any unauthorized use is strictly prohibited. Any product names, company names and logos mentioned or included herein are trademarks or registered trademarks of their respective owners.

Aumni, Inc. (“Aumni”) is a wholly-owned subsidiary of JPMorgan Chase & Co. Access to the Aumni platform is subject to execution of an applicable platform agreement and order form and access will be granted by J.P. Morgan in its sole discretion. J.P. Morgan is the global brand name for JPMorgan Chase & Co. and its subsidiaries and affiliates worldwide. Aumni does not provide any accounting, regulatory, tax, insurance, investment, or legal advice. The recipient of any information provided by Aumni must make an independent assessment of any legal, credit, tax, insurance, regulatory and accounting issues with its own professional advisors in the context of its particular circumstances. Aumni is neither a broker-dealer nor a member of any exchanges or self-regulatory organizations.

383 Madison Ave, New York, NY 10017