KPIs: To collect or extract? How venture firms can optimize for portfolio company experience

.jpeg)

Creating a process to gather and track KPIs from your portfolio companies can seem straightforward. But there are some key considerations to keep in mind.

Company KPIs are qualitative and quantitative metrics that allow investors to measure and evaluate company performance over time. KPI data can be collected, via surveys or reporting software; extracted, via review of financial statements or similar; or a hybrid approach that combines both methodologies. This article will cover the benefits of each approach so you can make an informed decision.

Fundamentally, there are three parties involved in an outsourced KPI collection or extraction process: venture firms, portfolio companies, and vendors. In all processes whether internally managed or with a vendor, venture firms are the end users of the data.

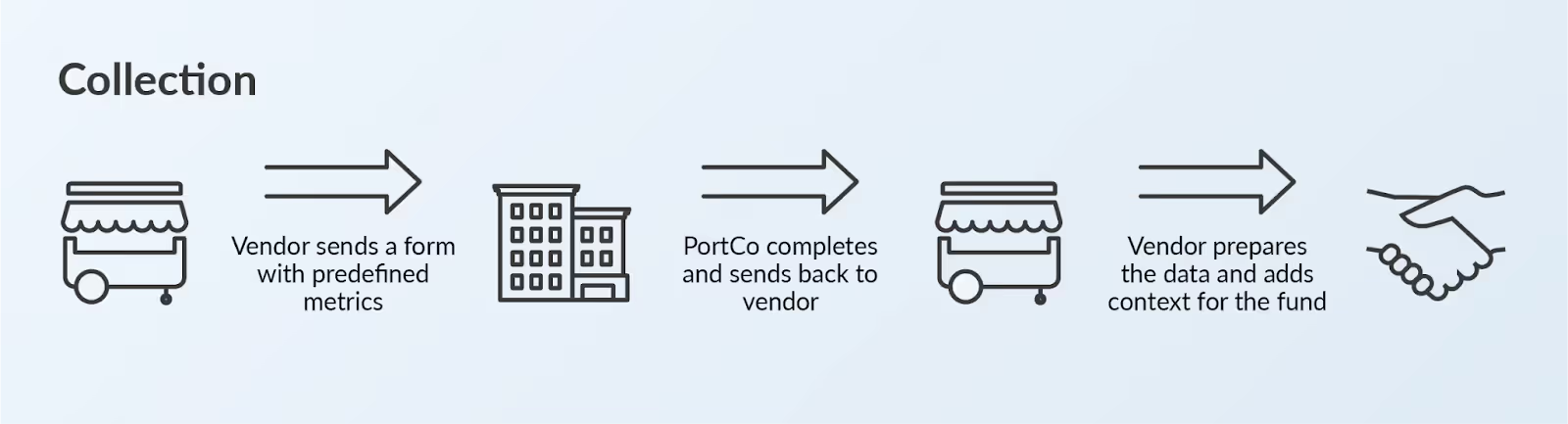

KPI Collection gathers data points directly from PortCo leadership teams. This means companies provide a predetermined set of data points to a vendor who then consolidates and edits on behalf of the venture firm.

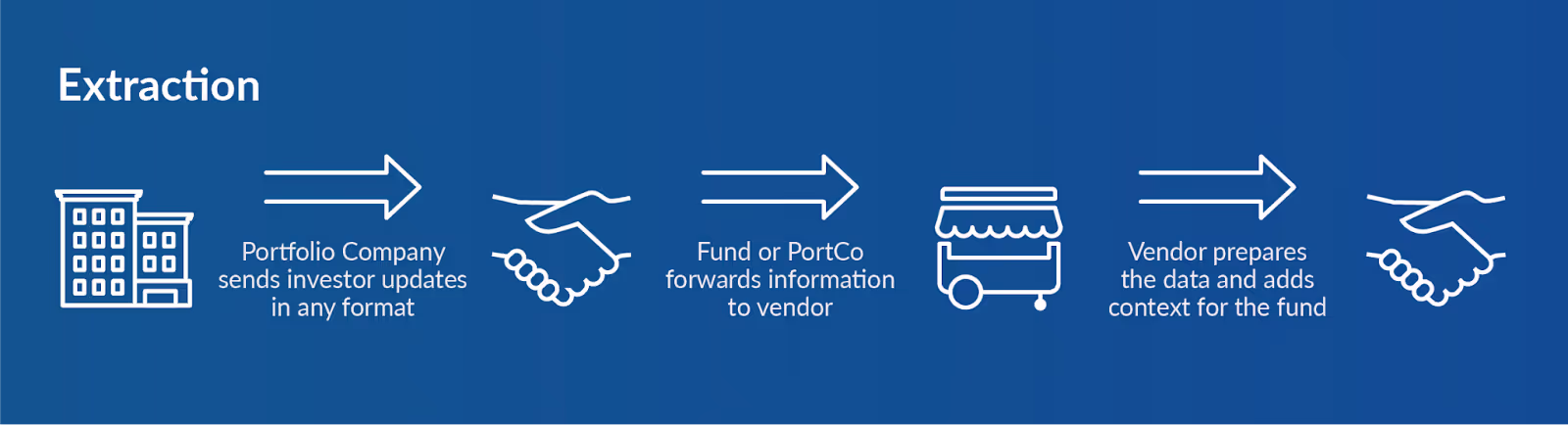

KPI Extraction is the process of gathering and extracting data points from investor updates (board decks, financial statements, investor emails, etc.) and then providing that data in structured form to the firm. This means the portfolio company doesn’t have to respond to the vendor with specific metrics.

So, what makes sense for your firm? Collection? Extraction? Both? Let’s drill into each and talk about the benefits and tradeoffs.

KPI Collection

Collection is the default answer for most firms. It is often considered the most straightforward way to obtain company performance metrics. After all, founders and their teams often have much of the data needed by investors on hand, so gathering exact data points from them seems like an obvious choice. That said, collection is better suited for certain use cases.

Excellent for Customized Reporting

We find most firms have a default list of industry standard metrics that are universally useful, such as:

- Revenue (or ARR)

- Cash on Hand

- Net Burn Rate

- Runway

- Headcount

- WAU/MAU

- Net Burn Rate

But what about more subjective metrics, such as ESG or DEI metrics? We find that most pre-built investor documents contain basic financial and operational metrics, but can be inconsistent or less reliable when it comes to data covering DEI or ESG metrics, complex financial ratios (e.g., LTV:CAC), or contextualized updates from founders.

This is where a KPI collection form shines. Venture teams can select the KPIs that are important to them from a library of metrics, including yes/no and open-ended questions. This gives teams additional context otherwise not possible when purely extracting data from standard investor reporting assets. For example, what if WAU is down by 40% because of a technical issue? What about an open headcount that remains unfilled, but they are closing the perfect candidate soon? Collection provides open-ended inputs for portfolio companies to provide context behind the number.

Cadence is Customizable

Investor updates from portfolio companies can be sporadic. With a KPI vendor, the collection process is a customizable form that can be delivered on a predefined cadence. We find 90%+ of firms default to a quarterly cadence, which helps keep the flow of data consistent without overburdening portfolio companies.

The Downside: Collection Can Create Friction

Founders are busy, and asking them or their teams to share data can produce mixed results. Response rates will vary depending on the relationship you have with the founder, information rights, board seat status, timing, and more. We’ve found that intro emails, context sharing, and other steps can help improve the outcome but completing a collection form will require a bit more lift by portfolio companies.

KPI Extraction

Extraction has obvious upside: simply forward the information you receive from the PortCo, format-agnostic, to a vendor. But here’s the more nuanced picture.

Extraction Removes the Burden from Founders

By forwarding existing resources, you eliminate the need to ask (and remind) founders to report on KPIs directly. It also provides founders the opportunity to submit updates and documentation they feel comfortable providing, in a format they prefer, without having to reiterate or restate information in a customized form. This removes reporting obstacles that can otherwise cause friction between founder-investor or reporting slowdowns. Maintaining founder relationships is the top factor firms consider when choosing extraction.

Working Around Info Rights

Extraction is the simplest way to get the data from decks and other assets into a usable format for firms without information rights. We find that most investors, regardless of their typical check size or rights, receive these assets in some form making extraction the straightforward choice.

Increased Auditability

Extraction–specifically when extracting metrics from financial statements–creates a robust audit trail because the process includes storage of investor-provided updates and documents in one place. This makes audits simpler than when information is spread across various document and data storage systems.

The Downside: Rigid

Extraction offers limited flexibility. Put simply: if a board deck and financial statement provide four out of the ten metrics you report on, you’ll only have 40% of the performance metrics you may need. When multiplied over many investments, this can create incongruity with the KPIs you have across the fund.

Venture KPI Collection & Extraction

We find that >50% of firms take a hybrid approach of both collection and extraction for many of the reasons listed above. Implementing both strategies ensures you receive comprehensive company metrics needed for valuations, reporting, and modeling workflows, while limiting the impact to founders. In our experience, it’s common to see extraction capture, say, 3 out of 8 key metrics. But collection processes complete the dataset with a quarterly outreach that collects the remaining 5 metrics from the portfolio company.

Edge Cases

Passive vs. Active Strategies VC KPI Strategies

Active investment strategies are the most dependent on a holistic KPI dataset due to hands-on role guiding and supporting founding teams. They need frequent performance reporting to execute effectively. Passive fund strategies generally rely more on extraction.

Number of Active PortCos

We find there is a relationship between firms with more active portfolio companies choosing extraction. Larger funds with portfolios of hundreds of investments often rely on extraction as the collection process can be difficult to scale.

Regulatory Requirements

LPs and state entities may also require specific metrics. A great example of this is California Senate Bill 54.

Wrap Up

There are myriad factors in determining the right strategy for your firm. Collecting KPIs generates the most complete datasets, but leans on founding teams. Extraction limits the time investment from a company, but doesn’t always provide all of the data the firm is looking for, especially if seeking uncommon metrics. Striking the right balance between the two approaches is paramount to ensure a positive PortCo experience and excellent KPI data.

Want to learn about how Aumni can help collect, organize and store KPI metrics?

You may also like: What KPIs do venture firms care about across stages?

.avif)

.avif)

©2025 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC.

This material is not the product of J.P. Morgan’s Research Department. It is not a research report and is not intended as such. This material is provided for informational purposes only and is subject to change without notice. It is not intended as research, a recommendation, advice, offer or solicitation to buy or sell any financial product or service, or to be used in any way for evaluating the merits of participating in any transaction. Please consult your own advisors regarding legal, tax, accounting or any other aspects including suitability implications, for your particular circumstances or transactions. J.P. Morgan and its third-party suppliers disclaim any responsibility or liability whatsoever for the quality, fitness for a particular purpose, non-infringement, accuracy, currency or completeness of the information herein, and for any reliance on, or use of this material in any way. Any information or analysis in this material purporting to convey, summarize, or otherwise rely on data may be based on a sample or normalized set thereof. This material is provided on a confidential basis and may not be reproduced, redistributed or transmitted, in whole or in part, without the prior written consent of J.P. Morgan. Any unauthorized use is strictly prohibited. Any product names, company names and logos mentioned or included herein are trademarks or registered trademarks of their respective owners.

Aumni, Inc. (“Aumni”) is a wholly-owned subsidiary of JPMorgan Chase & Co. Access to the Aumni platform is subject to execution of an applicable platform agreement and order form and access will be granted by J.P. Morgan in its sole discretion. J.P. Morgan is the global brand name for JPMorgan Chase & Co. and its subsidiaries and affiliates worldwide. Aumni does not provide any accounting, regulatory, tax, insurance, investment, or legal advice. The recipient of any information provided by Aumni must make an independent assessment of any legal, credit, tax, insurance, regulatory and accounting issues with its own professional advisors in the context of its particular circumstances. Aumni is neither a broker-dealer nor a member of any exchanges or self-regulatory organizations.

383 Madison Ave, New York, NY 10017